It’s a complicated relationship.

Americans depend heavily on their credit cards. And for the most part, they say they’re happy with the ones they have. Yet many are already looking for their next credit card.

A new CardRatings.com survey revealed that while most customers say good things about their credit cards, they’re also ready to move on. With credit card debt at record highs and many consumers falling behind on their payments, the next choice they make could have a lasting impact on their financial health.

Knowing when it’s time to find a new credit card and what to look for when choosing one can help you use your cards more successfully.

Consumers give their credit cards high grades

For most Americans, credit cards are a part of everyday life. The Consumer Financial Protection Bureau (CFPB) estimates that over 200 million adults in the United States have a credit card. That’s more than three-quarters of the adult population. Since most of those people have more than one card, there are nearly 800 million open credit card accounts in the United States.

The annual volume of purchases with these cards has risen to over $3 trillion. That represents about 46.4 billion separate transactions, meaning that on average, consumers use their credit cards hundreds of times a year.

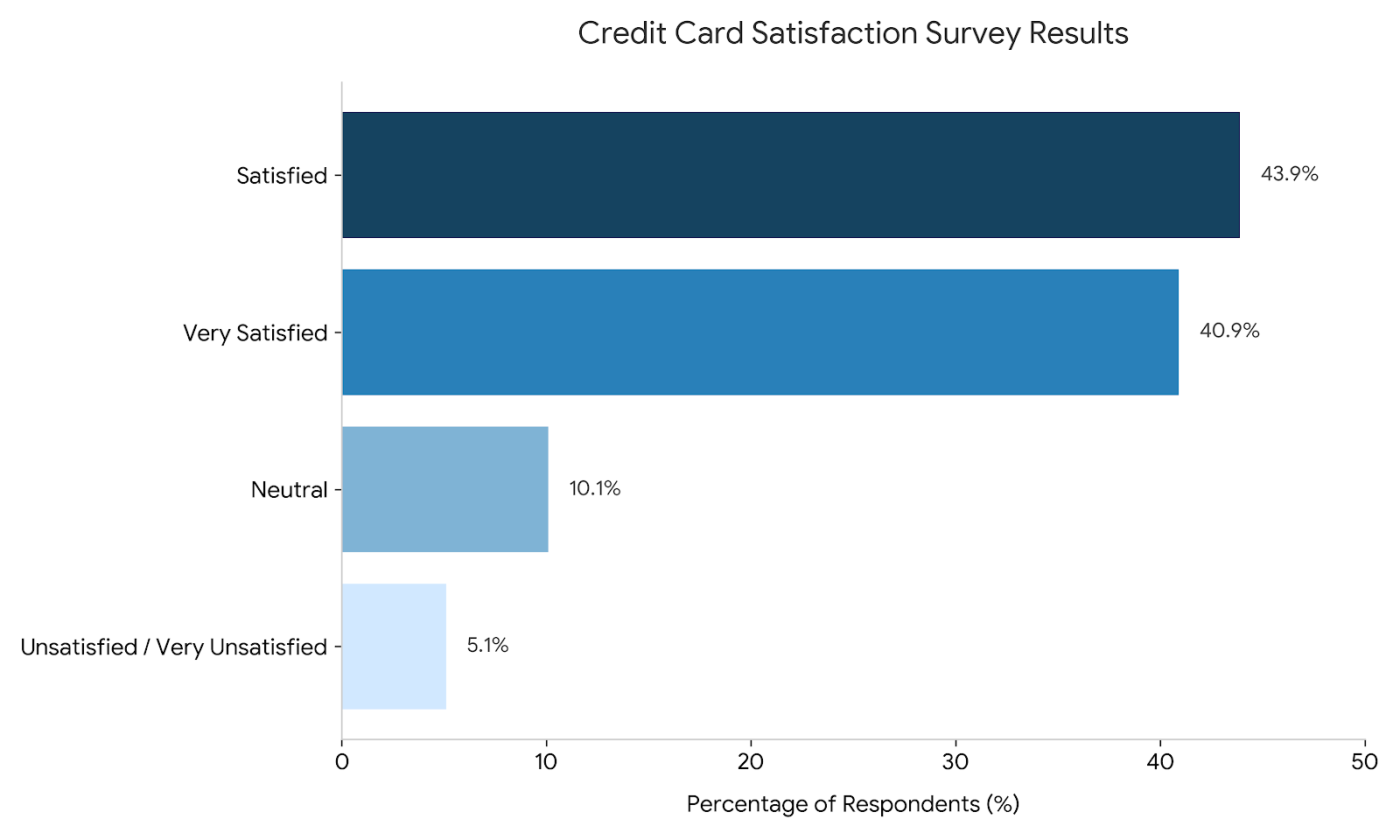

With people using their credit cards so much, they are in a good position to evaluate the performance of those cards. Overall, the survey found that respondents gave their cards high grades.

Forty-one percent of respondents said they were very satisfied with their credit cards. Another 43.9% said they were satisfied. With 10.1% saying they had neutral feelings about their cards, that left just 5.1% who said they were unsatisfied or very unsatisfied.

This makes it seem as though credit cards are generally doing a good job for their customers. And yet, many of those customers seem to have a nagging feeling that they could do better.

Despite high satisfaction, people are open to new opportunities

A total of 40.5% of survey respondents said they think there’s a better card out there for them. Another 40.2% said they were unsure, meaning they felt there might be a better card than the ones they have.

Just 19.3% of respondents said they were certain there was no better card for them.

With so many people feeling they could do better than their current credit cards, it wasn’t surprising to find that more than half of survey respondents (55.9%) said they planned to apply for a new credit card within the next year.

In short, people may like the credit cards they have, but they still have their eyes open for new opportunities.

When should you look for a new credit card?

This openness to checking out new credit card opportunities can be healthy. It’s a competitive market, with lots of choices. Plus, economic conditions change all the time, and so do household finances.

Even if you’re satisfied with your current cards, these six factors are strong indicators that a better, more rewarding option might be available

- When your card raises fees. Annual fees are especially important because you incur them no matter how you use the card. If you have other fees you’re regularly charged, you should also consider any increase in those as a cue to shop around. Weigh the benefits of the card against the fees you’re paying to make sure it’s still worthwhile.

- When your card raises your interest rate. This matters a great deal if you regularly carry a balance on your card. Interest rates change fairly often. Just because your card had a competitive rate when you signed up doesn’t mean it’s still competitive now.

- If your card cuts your credit limit. Some credit card companies may cut the amount of credit available to customers if the economy worsens. You may also see your credit limit cut if your credit score drops significantly. If your credit limit is no longer high enough to meet your needs, you may have to look for alternatives.

- If your spending habits change. What you buy can affect the rewards that you earn. It makes sense to have a credit card that gives generous rewards for things you tend to buy a lot of. If your spending habits change, you might find that a different card would earn you better rewards.

- If your payment habits change. The size of the balances you tend to carry on a credit card matters to what type of card suits you best. If you tend to carry large balances, finding the lowest interest rate you can matters a great deal. If you plan on paying your balance off in full each month, the interest rate won’t make a difference. In that case, you can focus on other card features, such as the size and type of rewards they provide.

- If you have a big change in your credit score. The credit terms a card gives you often depend on your credit score. This can affect your interest rate and the size of your credit limits. If your credit score moves up or down by a lot, a different card may be more competitive for someone with your updated score.

Even without any of these occurrences, it’s not a bad idea to check out the market at least once a year, to see what it has to offer.

➤ SEE MORE:Best credit cards of July 2026

What to look for when shopping for a new credit card

Here’s a checklist of what to look for when shopping for a new card:

- Annual fees. If a card charges an annual fee, you should think carefully about whether the benefits the card provides justify that fee.

- Interest rates. The higher the balance you’re likely to carry, the more important the interest rate is to your choice of a card.

- Credit standards. If you have great credit, you can pretty much take your pick of credit cards. If you have a lower credit score, not all cards may be available to you. Also, some cards have more competitive terms for lower credit score customers than others.

- Rewards. The more you use your credit card, the more important rewards become in your decision. Three things matter with rewards: the size, the types of purchases that earn the biggest rewards, and the type of rewards you earn.

- Apps and other digital tools. Besides financial terms, cards vary in the type of tools they offer to help you manage your account. The importance of this depends on both how you use technology and how you manage your finances.

Ultimately, the goal isn’t just to add another card to your wallet, but to ensure any new addition offers clear, incremental value. While it’s wise to be selective—as new applications can temporarily impact your credit—don’t let that stop you from upgrading. By making a direct comparison of the features that matter most to you, you can move forward confident that your next card is a meaningful improvement over the status quo.