While rewards credit cards make it easy to earn points or cash back on everything you buy, there are other money-saving opportunities to know about. For example, American Express, Capital One and Chase all run their own card-linked “offers” programs that can help you earn statement credits or bonus cash back on eligible purchases.

All you need to take advantage is a credit card from one of these issuers and an online or mobile account so you can check for deals. From there, you’ll find myriad ways to maximize Amex Offers, Capital One Offers, and Chase Offers with little effort on your part.

Understanding credit card “offers” programs

“Offers” programs from card issuers are merchant-funded deals you can activate and use to boost your rewards. When you activate an offer and make a qualifying purchase, you’ll typically earn a statement credit, bonus cash back, or extra rewards points.

Unlike coupon codes, these offers are automatically applied when you use your eligible card — no promo codes or screenshots required. However, you have to activate each offer or add it to your card before you shop. Every deal also comes with specific rules that must be followed for bonus rewards to apply.

Offers may vary by card, cardholder, and timing, which is why two people with the same card can see different deals in their accounts. Some offers are incredibly valuable with the potential to save you hundreds of dollars on eligible purchases, while others are only worth a few dollars a pop.

The good news about Amex Offers, Capital One Offers, and Chase Offers is that these programs are free and easy to use. Also, rewards or statement credits you get come on top of the rewards you earn by paying with a credit card.

How does Amex Offers work?

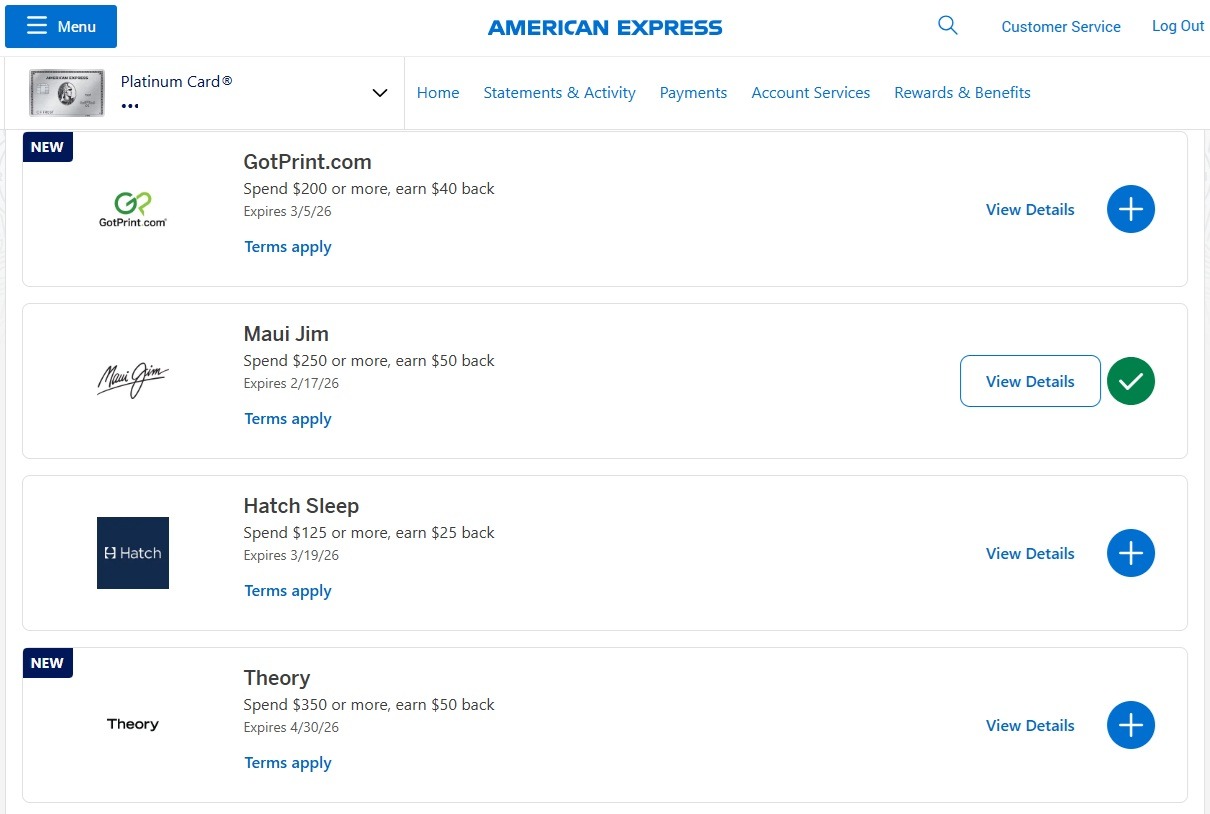

American Express Offers are available in your online Amex account or the issuer’s mobile app, and they tend to be fairly valuable. While these offers come from thousands of retailers, travel providers, and restaurants, you will find dozens of available offers in your account at any given time. Amex card offers change frequently, but some available offers right now include:

- CNN: Spend $6.99 or more, earn $6.99 back, up to 3 times (total of $20.97)

- Cruise America RV Rentals: Spend $500 or more, earn 10,000 Membership Rewards points

- Maui Jim: Spend $250 or more, earn $50 back

- Viator: Spend $325 or more, earn $35 back, up to 2 times (total of $70)

To take advantage of an offer, you need to read the fine print and understand the rules. From there, you’ll click on the side of the offer to activate it, which reveals a green checkmark.

Once you add an offer to your card, you simply make a qualifying purchase with that card before the offer’s expiration date. Statement credits typically post within a few days to a few weeks.

One important thing to know about Amex Offers is that they are card-specific, not account-wide. If you have multiple Amex cards, you may see the same offer or a variation of an offer appear on more than one card. Some offers can also be used more than once on the same card, but only if you meet purchase requirements and make all eligible purchases before the offer’s expiration date.

How does Capital One Offers work?

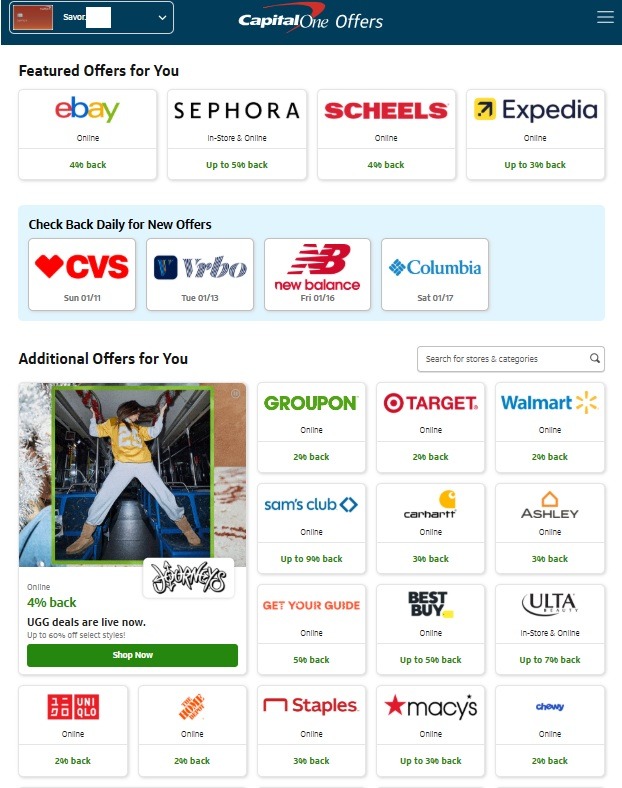

Capital One Offers works a little differently since most are tied to online shopping and cash back. Then again, you can earn bonus miles on eligible Capital One Offers purchases if you have a travel credit card like the Capital One Venture Rewards Credit Card or Capital One Venture X Rewards Credit Card.

Regardless of the card you have, you’ll access Capital One Offers shopping through your online account or browser extension. When you click through to an eligible merchant from the Capital One Offers portal and complete your purchase, you’ll earn cash back or miles that are tallied separately from your credit card rewards.

Examples of Capital One offers available right now include:

- Instacart: up to 7% cash back

- Lowe’s: 2% cash back

- Sephora: up to 5% cash back

- VRBO.com: 3% cash back

Similar to Amex Offers, Capital One Offers is card-specific. This means you may have different offers available for different Capital One credit cards you have, and that you can stack more than one deal when that’s the case.

How does Chase Offers work?

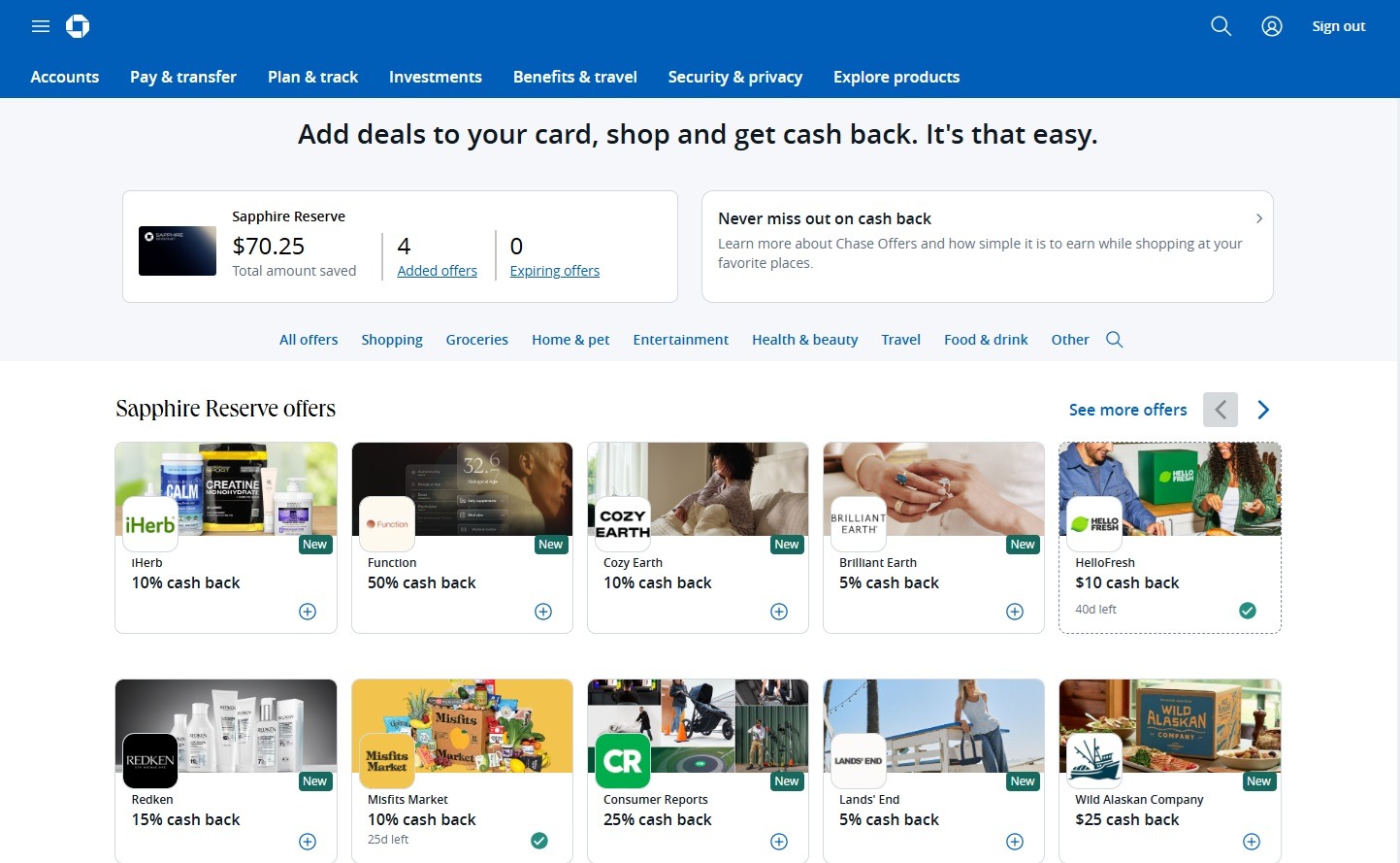

Chase Offers sits somewhere between Amex and Capital One in terms of simplicity, with common categories including dining, travel, groceries, and subscription services. These offers come in the form of statement credits or bonus cash back tied directly to your Chase rewards credit card.

You’ll find Chase card offers by logging into your Chase account or the Chase mobile app and selecting a specific card. Like Amex Offers, Chase Offers must be activated before use, and each offer includes spending requirements and exclusions.

Examples of current Chase offers include:

- Hello Fresh: $10 cash back on your first three payments ($30 maximum)

- Misfits Market: 10% cash back on eligible purchases ($20 maximum)

- Paramount+: $4 back on your Paramount+ subscription when you spend $4 or more, including taxes and after any discounts

- Ruggable: 15% cash back on your Ruggable purchase, including taxes and after any discounts ($50 maximum)

Chase Offers are usually less flashy than Amex Offers, but they can still add up — especially if you’re already spending at the participating merchants. As with Amex and Capital One, Chase Offers are card-specific. You may see different offers on different Chase cards, even within the same account.

Best ways to maximize credit card “offers” programs

Knowing these programs exist is half the battle. However, the real savings comes from using “offers” programs strategically and as often as you can. Here are the most effective ways to squeeze maximum value out of Amex Offers, Capital One Offers, and Chase Offers over time.

Activate offers before you use them

This tip probably sounds obvious, but it’s the most common mistake people make. If you don’t activate the offer first, you won’t earn the credit or bonus — no exceptions.

Make it a habit to scroll through your available offers regularly and add anything that looks remotely useful. You don’t need to use every offer you activate, but this helps ensure that you won’t miss out if you do end up making a qualifying purchase.

Read over the fine print and exclusions

Every offer comes with terms, and ignoring them can cost you real money. Pay close attention to:

- Minimum spending requirements

- Eligible purchase channels (online only, in-store only or both)

- Excluded products or brands

- Whether taxes, fees, and shipping count toward the total

For example, an offer might require a single purchase of $100, not multiple smaller transactions. Others may only work on U.S. websites or exclude third-party sellers. In any case, a quick look over of the fine print can save a lot of frustration later.

Check for new deals regularly

Credit card offers are constantly changing. Some appear for a few weeks, while others disappear quickly or get replaced by new deals.

American Express, in particular, frequently adds new offers without notice. On the other hand, Capital One deals tend to come from the same companies over and over, which may benefit you if you’re a regular shopper at one or more of the program’s participating stores.

Regardless of which program you use, set a reminder to review your offers at least once per week. You may even want to check in more often if you’re an active card user, or if you frequently find deals you can use.

Look for different offers for different cards

If you have multiple cards from the same issuer, compare the offers on each one before you shop. You might see a highly sought-after offer on multiple cards you have, giving you the option to take advantage of it more than once.

You might also see:

- A higher spending threshold on one card

- A better statement credit on another

- A bonus points offer that makes more sense for your goals

Choosing the right card for the right offer can significantly increase your savings, especially for larger purchases.

Split purchases (when it makes sense)

Sometimes, splitting up a purchase can help you trigger multiple offers. However, this only works in specific situations.

If you have two Amex cards with the same “Spend $50, get $10 back” offer, for example, splitting a $100 purchase into two $50 transactions could earn you $20 back instead of $10.

That said, not all merchants allow split payments, and some offers require a single transaction. Always check the terms and be realistic about whether this strategy is worth the effort.

Stack credit card “offers” with shopping portals

You should also make sure you’re stacking credit card offers with online shopping portals.

Here’s how it can work:

- Activate an Amex or Chase Offer

- Click through an online shopping portal (like Rakuten or the Chase shopping portal)

- Use the eligible credit card to pay

When you’re able to stack offers, you can typically earn cash back or a statement credit through the “offers” program, bonus rewards for shopping through a portal, and the normal rewards you earn with your credit card. Stacking doesn’t work with every offer, but the savings can be substantial when it does.

Use the right rewards credit card

Also make sure you’re using the optimal rewards credit card for every purchase, or the one that will earn the most rewards for what you plan to buy. If you are taking advantage of Chase card offers for restaurants, for example, you should try to use the offer with a Chase card that earns bonus rewards on dining. If you are after a travel offer, on the other hand, cards that earn more rewards on travel purchases can fit the bill.

Using the right card can make sure you earn the most rewards possible on your card and through the merchant offer at the same time.

➤ SEE MORE:Best credit cards for online shopping

Bottom line

Amex Offers, Capital One Offers, and Chase Offers don’t require advanced knowledge of points or miles, complicated redemptions, or loyalty to a single brand. These programs only require some awareness and consistency, which most card users can handle.

By activating offers early, reading the fine print, checking for new deals regularly, and stacking strategically, you can turn everyday spending into easy savings. Over time, these small wins can add up to hundreds of dollars back in your pocket each year.